Two months into the RSP-led government, I find myself reflecting not only as a critic but also as a citizen who wants this political movement to succeed.

My critique of the Prime Minister and this government does not come from hostility. It comes from expectation. I want them to do well because their success would mean something better for Nepal.

There is undeniable hope among ordinary people right now. You can hear it in everyday conversations and see it in the growing frustration with the past 35 years of Congress and UML politics. That frustration has turned into a strong desire for change. At the same time, this hope is also being shaped by populist narratives. Some are clearly benefiting from this mood. This tension deserves careful attention rather than blind support or easy dismissal.

We also need to stay grounded in reality. The people now in power did not come into politics because they had already proven themselves in governance. They came as alternatives. That creates an opportunity, but it also brings responsibility. The recent Human Rights Commission report is a reminder that performance must be examined carefully and not assumed.

As a teacher, I have learned something important over the years. The students who question me the most at the beginning of a semester often become the ones who understand my work best by the end. Questioning, when it is taken seriously, builds trust. Silence does not.

I approach this government in the same spirit. Questions are not threats. They are part of accountability. People who speak should not be feared. What should concern us is the culture of silence that has shaped much of our political leadership, including the current Prime Minister.

I remain critical, and I remain hopeful.

For the sake of all those who continue to believe in the possibility of change, I sincerely wish this government success.

A group from Montreal is about to spend $500 million buying up unsold condos across the GTA—often at about half the original presale price. These are the very projects that many of our people walked away from after pouring in hard‑earned savings, assignment fees, and years of waiting. Now, the same “problem” that broke individual buyers’ backs is being treated as a “golden opportunity” for big investors.

For months, we watched neighbours cancel assignments, forfeit deposits, and quietly admit defeat. Some families had to choose between sinking more money into overpriced units or walking away with nothing. Many chose the latter—not because they didn’t want to own, but because the market turned against them. Yet, when ordinary people retreat, institutions step in with deep pockets, buying in bulk at deep discounts.

This is not just a real‑estate story. It’s a story about who bears the risk and who reaps the reward. When the market booms, the fantasy is sold to small investors, diaspora families, and first‑time buyers. When the bubble cools, those same buyers are left holding the losses, while corporations quietly acquire entire buildings as “value plays.” Our fear, our stress, our sacrificed savings become their balance‑sheet assets.

What’s even more troubling is what this signals for the future. Those who can buy at half‑price today will likely rent the units back to us at market‑rate or higher tomorrow. Instead of a market correction that brings affordability, we may simply get a transfer of power—from overstretched buyers to consolidated landlords. Public policy and housing regulations have done little to intercept this process. Housing is being treated as a financial instrument, not as a basic human need.

For our community, this moment should be a wake‑up call. We need to stop seeing every presale project as a guaranteed “investment” and start asking: Who really benefits when we are forced to walk away? We need to push for policies that protect small buyers, cap speculative land banking, and ensure that when the market crashes, ordinary people are not left alone to pay the price.

This is not just about losing money in a condo deal. It’s about who controls housing, who gets bailed out, and who gets erased from the story. If we don’t speak up now, our pain today will be written off as “market correction” in textbooks—while the profits quietly go to those who knew exactly when to buy at the bottom.

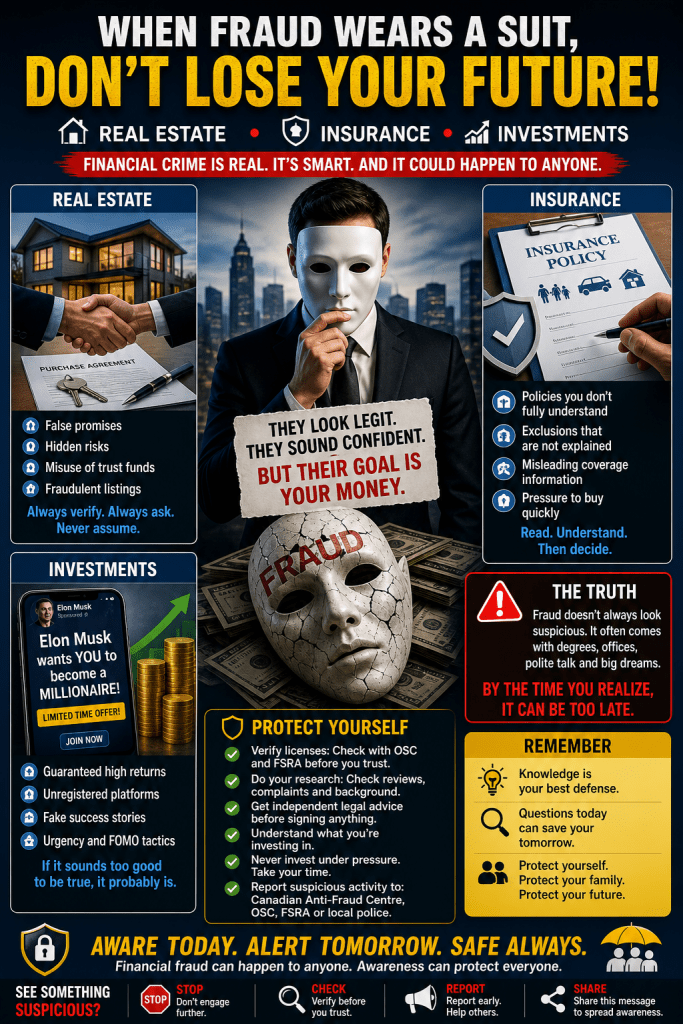

What would you do if your life savings disappeared not through a robbery, but through documents you believed you could trust?

Across the Greater Toronto Area and beyond financial crime is becoming harder to see and easier to fall into. It no longer happens in dark alleys. It moves through contracts investment pitches and professional networks that appear legitimate on the surface. Some of the most damaging crimes today wear suits speak confidently and promise opportunity.

What makes this even more concerning is how risk now cuts across industries we normally trust Insurance real estate and investment spaces are not immune. Whether it is a policy that is not fully explained a property deal that hides risk or an online investment promising life changing returns the pattern is often the same. I came close to falling into one of these traps myself. A few years ago I saw an online promotion claiming that Elon Musk wanted Canadian ordinary people to become millionaires through a limited opportunity. It looked convincing professional and urgent. That is exactly how these schemes work not by appearing suspicious but by appearing credible.

Financial fraud is not victimless, and it is rarely obvious. In Ontario patterns have emerged through warnings and reported cases. Misuse of real estate trust funds high risk promissory notes marketed as safe mortgage fraud through misrepresentation and unregistered investment schemes are becoming more visible. Vulnerable groups including seniors newcomers and those unfamiliar with financial systems are often targeted. Organizations like the Ontario Securities Commission and the Financial Services Regulatory Authority of Ontario continue to issue alerts, yet many people only encounter these warnings after losses occur.

There is also a growing frustration that nothing seems to happen when financial crime occurs. The truth is more complex. These cases involve extensive documentation multiple actors and the challenge of proving intent. Investigations take time and legal thresholds are high. This creates a gap between public expectation and visible accountability. That gap slowly erodes trust and discourages victims from speaking out.

Behind every case there is a human story. Financial fraud takes more than money. It takes security dignity and peace of mind. People have lost retirement savings home equity compensation funds and years of stability. Victims are not reckless. Many are careful people who believed they were making responsible decisions. Families trying to build a future seniors seeking stability and newcomers trying to navigate a new system often carry the heaviest burden.

Unlike street crime financial fraud hides behind legitimacy. It uses complex paperwork, legal language trusted intermediaries, and emotional connection. It often relies on urgency and familiarity. By the time doubt appears the damage is already done.

There are warning signs that should never be ignored. Promises of high returns with little risk pressure to act quickly lack of transparency unverified professionals and appeals based on trust or community. If something feels rushed or unclear it is worth pausing. That pause can protect everything you have worked for.

In a complex financial environment awareness becomes your strongest protection. Verifying credentials through the Ontario Securities Commission or the Financial Services Regulatory Authority of Ontario seeking independent legal advice and asking direct questions are no longer optional steps. They are necessary habits. Reporting suspicious activity to organizations like the Canadian Anti-Fraud Centre also helps protect others.

This is not about creating fear. It is about closing the gap between trust and understanding In fast growing regions like the Greater Toronto Area opportunity and risk move together. Fraud thrives where awareness is low and blind trust is high.

A healthy society does not rely only on punishment after damage is done. It builds people who can recognize deception before becoming victims. When fraud wears a suit awareness becomes the first line of defense.

Before trusting a financial promise remember that due diligence is always cheaper than regret.