I recently watched a podcast by mortgage expert Ron Butler discussing a troubling trend in Ontario’s real estate market: home purchase failures have increased by 500% compared to pre-COVID levels.

That number should make all of us pause.

What Is a “Purchase Failure”?

A purchase failure happens when a buyer signs a contract to buy a home — new construction or resale — but cannot close the deal on the agreed closing date.

In simple terms: The buyer doesn’t have the money or cannot secure the mortgage needed to complete the purchase.

Before COVID, less than 1% of purchases failed. Today, that number is reportedly around 5% — and in new construction, some estimate it could be much higher.

Why Are Deals Falling Apart?

There are several major reasons:

1. Appraisal Problems (Especially New Construction)

Many buyers purchased pre-construction homes or condos in 2021–2022 at peak prices. Now that projects are completing:

Market values have dropped.

Appraisals are coming in far below the original purchase price.

Buyers must cover the difference in cash.

If you bought at $1.95M and the appraisal comes in at $1.525M, that’s a $400,000 gap you must cover. Many simply can’t.

2. Condo Market Reality

Some buyers purchased condos years ago at inflated prices, expecting appreciation or easy rental income. Today:

Comparable units are selling for less.

Higher interest rates mean negative monthly cash flow.

Rental income often doesn’t cover mortgage payments.

Some buyers are choosing to walk away from large deposits rather than close on a losing investment.

3. Mortgage Qualification Issues

In resale markets, failures are happening because:

Buyers couldn’t sell their existing home for the expected price.

Income was overstated or improperly assessed.

Job losses occurred before closing.

Buyers assumed pre-approvals guaranteed final approval (they don’t).

As Ron Butler bluntly stated: “The buyer doesn’t have the money.”

Why This Matters to Our Community

This is not about panic. It’s about awareness.

When purchase failures rise:

Sellers face uncertainty.

Builders face stress.

Buyers risk losing deposits.

Legal disputes increase.

Financing becomes stricter.

We are entering a market where leverage cuts both ways.

For years, rising prices hid risk. Today, falling values expose it.

If You’re Buying or Investing, Be Careful

Before signing anything:

Get a fully verified mortgage approval (not just a quick pre-qual).

Be conservative with projected sale prices.

Stress-test your finances at higher interest rates.

Understand appraisal risk.

Have liquidity reserves.

Read pre-construction contracts very carefully.

Speculation worked in a rising market. It is dangerous in a correcting one.

Final Thought

Real estate is not guaranteed to go up. It never was.

The goal is not to scare anyone — but to make sure our community members are informed. The people who survive market corrections are not the boldest. They are the most disciplined.

If you’re planning to buy, sell, or close on a property soon, now is the time to review your numbers carefully.

Canada’s housing crisis is often discussed in absolutes: either prices will crash, or they will never fall; either governments must intervene more, or get out of the way entirely. But when we place recent market conditions alongside deeper structural critiques—like those raised on Angry Mortgage—a more complicated, and more honest, picture emerges.

A Short-Term Opening for Buyers

In the near term, there is a meaningful shift underway—particularly in markets like Toronto and Vancouver.

Sales volumes are historically low. Investor activity has largely evaporated. Pre-construction is stalled. Buyers who remain are mostly end users: families and individuals looking for a place to live, not to flip. This has quietly shifted leverage. Selection has improved. Negotiation is back. Sellers, not buyers, are adjusting expectations.

This does not mean we are at the “bottom,” nor does it mean prices cannot fall further. But for financially stable households—especially first-time buyers who were entirely shut out between 2020 and 2022—this is the most buyer-friendly environment in years.

Yet this short-term opening exists inside a housing system that remains fundamentally broken.

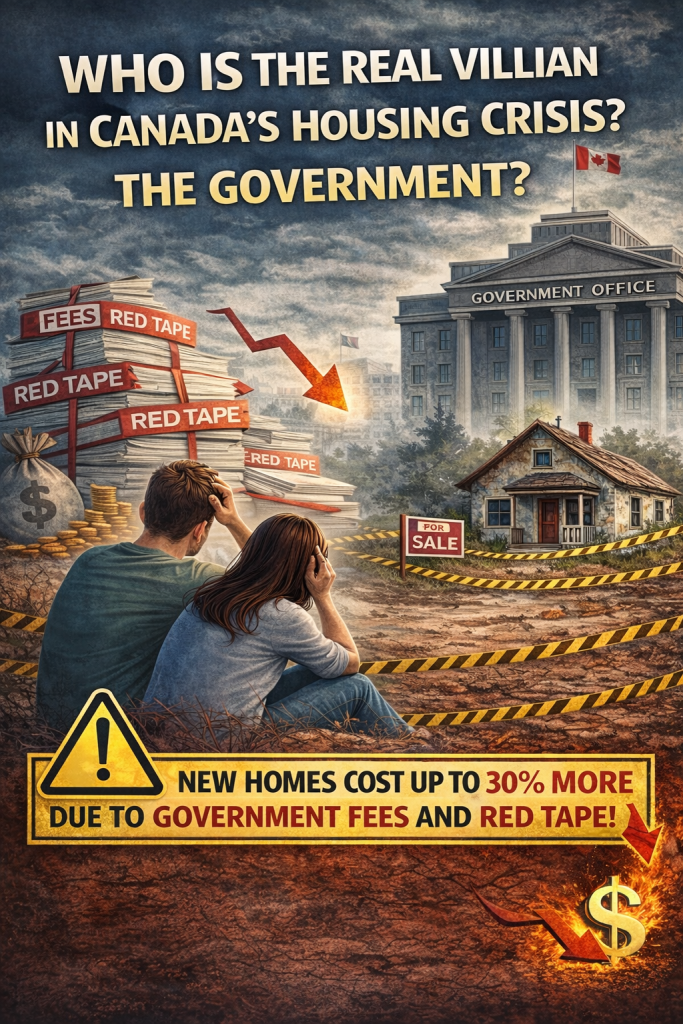

The Structural Problem: Housing as a Government Revenue Tool

As Ben Woodfinden argued on Angry Mortgage, the most under-discussed driver of unaffordability is not speculation alone, immigration alone, or even interest rates—but government cost-loading on new housing.

In cities like Toronto, as much as 30% of the cost of a new home is made up of development charges, fees, taxes, and levies. These are not marginal costs. They are embedded into the price of every unit, passed directly to buyers, and treated as a normal feature of governance.

Housing, in effect, has been taxed like a luxury good—while being rhetorically framed as a human necessity.

Layered on top is what Woodfinden calls the “Anglo disease”: a regulatory culture that makes building slow, adversarial, and legally dense. Years of approvals, consultant reports, appeals, and political veto points create scarcity by design. The result is not careful planning—it is paralysis.

This is how Canada ends up with 50-storey towers beside single-family zoning, and almost nothing in between.

The Missing Middle—and the Missing Social Contract

What ties these discussions together is not just economics, but expectations.

A generation of Canadians did what the social contract asked of them: education, work, saving, delayed gratification. Yet homeownership now requires top-1–2% household incomes in major cities. The promise that effort leads to stability has quietly collapsed.

That anger is not theoretical. It shows up in delayed families, longer commutes, overcrowding, and a growing sense that democracy responds faster to asset holders than to workers.

When young professionals earning $90,000–$100,000 cannot even imagine owning a modest home, something deeper than market cycles has failed.

So Where Does This Leave Us?

In the short run, today’s market offers cautious opportunity for buyers who are purchasing shelter, not status.

In the long run, affordability will not be restored without structural change:

Development charges must be rethought.

Zoning must allow mid-density housing where people already live.

Speed, not symbolism, must become the metric of housing policy.

More programs alone will not fix this. Nor will pretending the market can self-correct under the current regulatory load.

A Critical Outlook

Canada’s housing crisis is not caused by a single villain. It is the outcome of decades of policy choices that treated housing simultaneously as an investment vehicle, a revenue source, and a political risk to be avoided.

Buyers may find a window today—but unless governments stop profiting from scarcity while promising affordability, that window will close again.

The question is no longer whether housing is broken. It is whether we are willing to stop pretending we don’t know why.

I listened to today’s episode of Ron Butler’s Angry Mortgage Podcast, and the numbers he shared were not just bad—they were historic.

By the end of 2025, Canada’s two largest housing markets collapsed in terms of sales activity:

Vancouver recorded its lowest home sales in 20 years

Toronto (GTA) fell to a 25-year low

These aren’t just market fluctuations. They’re signals of a structural shift that many people—buyers, sellers, and real estate professionals alike—are still struggling to accept.

So, what went wrong?

According to Butler, the biggest reason is simple but uncomfortable: entire categories of buyers have vanished.

During the peak years (especially around 2021), as much as 40–45% of purchases in the GTA were investor-driven—landlords, flippers, speculators, short-term rental buyers. That group is now gone. Completely.

Buying a condo to rent? Buying a house as an “investment”? Those strategies no longer make financial sense in today’s environment.

And once that investor demand disappeared, the market lost nearly half of its fuel.

Prices fell—but that didn’t bring confidence back

Home prices in the GTA are now down roughly 25% from the March 2022 peak. But instead of encouraging activity, this decline has created paralysis.

Many potential sellers are stuck:

Selling now wouldn’t give them enough equity for their next purchase

After commissions and costs, moving simply doesn’t add up

Others fear selling today only to realize prices fall further tomorrow

As Butler puts it, why buy now if you believe you can buy the same house for $50K, $100K—or even $200K less next year?

Who’s left in the market?

At this point, Butler argues there’s really only one group left that might sustain activity: first-time home buyers.

They don’t need to sell a home first. They aren’t worried about losing equity. They’re looking for stability, schools, permanence—a place to call home.

But even they are hesitant.

Job uncertainty, economic unease, global instability, and constant “wait-and-see” messaging have made this a sentiment-driven freeze. Housing isn’t just numbers—it’s emotion. And right now, the emotion is caution.

Will foreign buyers save the market?

Short answer: no.

Even if restrictions ease, Butler notes that any reopening would likely apply only to new construction, not resale homes. That does little for today’s stalled market and won’t reverse the broader trend.

What about 2026?

Ron Butler is blunt:

Prices are still coming down

Don’t believe anyone who says the bottom is already here

If someone tells you “buy now or miss out,” his advice is simple: just say no

Eventually, affordability will improve enough that buyers step back in. But that doesn’t mean a quick rebound or a return to pandemic-era highs.

The bigger takeaway

This isn’t a crash fueled by panic. It’s a slowdown driven by reality.

The era of speculative excess is over—at least for now. What remains is a slow, difficult recalibration where housing slowly reconnects with wages, stability, and actual human needs.

For buyers, patience matters. For sellers, expectations matter. And for anyone promising a sudden turnaround—it’s worth listening carefully to voices like Ron Butler before believing the hype.

For the past few years, talking about real estate in Ontario—especially in the Greater Toronto Area—has felt like walking through a hall of mirrors. Prices up, prices down. Rates rising, rates cutting. Realtors shouting optimism, buyers frozen in fear, sellers clinging to yesterday’s peak.

As we step into 2026, one thing feels different: the noise is slowly fading, and reality is returning.

This is not a prediction of a boom. It is not a warning of a crash. It is something rarer—and healthier.

A Market That Is Finally Catching Its Breath

After years of extreme swings, the GTA market appears to be moving toward normalization.

Prices have already corrected from their 2021–2022 peaks

Speculative frenzy has largely disappeared

Buyers are no longer rushing blindly

Sellers are being forced to price realistically

This doesn’t mean homes are suddenly affordable for everyone. But it does mean the market is less emotional, less inflated, and less detached from income realities than it was a few years ago.

That alone is progress.

Interest Rates: Not Cheap, But Predictable

One of the biggest changes heading into 2026 is not ultra-low interest rates—it’s stability.

For the first time in years, buyers can plan without fearing sudden shocks. Mortgage rates may fluctuate slightly, but the era of constant surprises appears to be behind us. That predictability matters more than people realize.

Real estate markets don’t need cheap money to function. They need certainty.

With rates no longer rising aggressively, more end-users—not speculators—are slowly re-entering the market.

Buyers Are Wiser Than Before

2026 buyers are not the buyers of 2021.

They:

Ask questions

Compare neighborhoods

Negotiate

Walk away when numbers don’t make sense

This is a quiet but powerful shift. A market led by informed buyers is healthier than one driven by fear of missing out.

First-time buyers, in particular, may find 2026 less hostile—not easy, but less punishing—especially in condo and townhouse segments where inventory remains higher.

Sellers Will Need to Accept a New Reality

The hardest adjustment in 2026 may not be for buyers—it may be for sellers.

Many homeowners are still emotionally attached to peak-era prices. But the market no longer rewards hope; it rewards pricing aligned with today’s conditions.

Homes that are:

Well-priced

Well-maintained

Realistically marketed

will sell.

Others will sit.

This isn’t a crisis—it’s a correction in expectations.

Investors: A Different Game Now

For investors, 2026 is not about quick appreciation. The math is tighter, margins are thinner, and holding costs matter more than ever.

This is not necessarily bad. It filters out reckless speculation and favors:

Long-term thinking

Ethical rental practices

Cash-flow realism

Housing should not function only as a trading asset. A calmer investment environment ultimately benefits tenants, buyers, and communities.

What 2026 Really Represents

More than anything, 2026 looks like a reset year.

Not a return to the past. Not a dramatic collapse. But a slow rebuilding of trust between prices, incomes, and reality.

The GTA market doesn’t need excitement. It needs honesty.

And for the first time in a long while, honesty may be creeping back in.

A Final Thought

Real estate cycles punish excess and reward patience. The last cycle was built on urgency, leverage, and belief that prices only move one way.

2026 feels different—not because everything is fixed, but because illusions are fading.

For buyers, sellers, and observers alike, this may finally be a year to stop reacting—and start thinking.

And that, in the long run, is how healthier markets are built.

(Note: This post is based on the ideas of GTA real estate experts like Ron Butler, John Pasalis, Jon Flynn and other!)

Ron Butler from Angry Mortgage Podcast talks with Jon Flynn, a 21-year real estate veteran from Niagara, about how we got from normal housing prices to total insanity and back to crisis

When Jon Flynn started in real estate in 2004, a single family home in Niagara averaged $130,000. He remembers working with a busy realtor who accidentally countered an offer at $230,000 instead of $130,000. She laughed it off because she was “used to dealing with all these high-end homes.”

Twenty years later, those same modest homes peaked at unimaginable prices. Then they started collapsing. Flynn and mortgage broker Ron Butler traced exactly how this happened and why it will get worse before it gets better.

Phase 1: Vancouver Money Arrives (2015-2016)

The madness started when British Columbia blocked foreign buyers. Chinese millionaires who had been buying Vancouver real estate simply flew to Toronto instead. Their method was smart and legal. Send kids to Canadian universities. Get them PR status. Funnel money through them to buy property.

Toronto prices exploded. Within a year, the craze hit Niagara. Multiple offer nights became normal. Agents would line up buyers outside homes, check their prices, and literally tell them “Get out” if the number was too low.

Flynn says what happened in the GTA always arrived in Niagara about 12 months later.

Phase 2: Toronto Investors Invade (2016-2018)

Toronto homeowners discovered something. They could remortgage their appreciated homes, pull out equity, and buy cheaper properties in Niagara, Hamilton, and other regions. At first the rental math worked. You could rent to a family and break even.

But prices kept climbing beyond what rents could support. So investors switched to Airbnb. When cities cracked down on Airbnb, they pivoted to student rentals. When that collapsed, some literally chopped houses into pieces. Ten bedrooms in an 1,100 square foot house.

Each phase made less economic sense than the one before.

Phase 3: COVID Insanity (2020-2021)

Then COVID hit and things went completely crazy. December 2020 had the highest average home prices of the entire year. December is normally the slowest, lowest price month in real estate.

“That was a sign,” Flynn said. “Something was wrong.”

Ultra low interest rates. Work from home policies. Everyone believed office work was dead forever. Speculation hit levels nobody had seen before. GTA residents fled downtown condos where they waited an hour for elevators with three person limits. They bought everything available in suburban Ontario.

Butler remembers a client in Fort Erie who wanted to pay $700,000 for a basic bungalow. Butler asked why. The client said he had made $400,000 in real estate in the last two years. That was the thinking. Past gains justified any future price.

By 2021, every realtor rebranded as an investment expert. Social media made everything worse. Flynn made two and a half times his normal income that year. Butler made similar multiples. New realtors thought this was normal. They bought Hummers and multiple investment properties.

“Everybody and their brother and their mother were just buying houses,” Butler said. “It didn’t matter what you could rent them for. It didn’t matter what they were worth.”

Phase 4: The Student Explosion (2022-2023)

As interest rates rose and speculation cooled, a new distortion arrived. International students. Canada’s student visa approvals jumped from 172,000 nationally to 480,000 just in Ontario.

Private immigration consultant centers appeared everywhere. More than weed shops in Niagara Falls, Flynn said. Investors who couldn’t make money with families or Airbnb packed international students into houses.

Flynn described buses packed with students fighting to board. Security guards at Niagara College controlling crowds. Neighborhoods transforming overnight.

One story stuck with him. A realtor on his street sold a home to another agent who said her mother and daughter were moving in. On closing day, students with grocery bags stood on the porch. The house was soon chopped into 10 bedrooms.

The Collapse

By 2022, everything stopped. Interest rates spiked. Immigration policies tightened. The fundamentals that never existed could not be ignored anymore.

“Fundamentals are back,” Flynn said. “People want affordable family homes.”

Power of sales started appearing. First from reckless speculators. Now increasingly from regular homeowners. Each foreclosure creates a new, lower price. It drags down entire neighborhoods.

Both Butler and Flynn emphasize this point. What we see now in late 2025 comes from decisions made 9 to 12 months ago. The real pain from job losses has not fully hit yet.

“We haven’t really seen the families with job losses going into power of sale,” Butler said. “That’s the next wave.”

Where We Are Now

Flynn has listings at fair prices. Even below recent sales. Zero showings. One expensive listing had one showing in three months. The GTA investors who flooded Niagara during the boom have completely vanished.

Butler tracks regional numbers. Four Ontario regions are approaching average losses of $400,000 from peak prices. Vancouver and Calgary are grinding down too. The spring market showed no recovery in 2025.

“You cannot expect prices to go up this spring,” Flynn warned about 2026. “They might a little bit, but chances are they’re going to go down.”

The most sobering moment came when Flynn recalled 2012 and 2013. “I sold a house to a girl working as a shift manager at McDonald’s. Only one on title, only one on mortgage. Two people working at Tim Hortons bought a house. Legitimately, no fraud.”

Butler agreed. “When I started 30 years ago, ordinary people with absolutely average incomes were buying houses. Prices have not fallen anywhere near enough for that to come back.”

The Honest Assessment

Neither Butler nor Flynn sugarcoat the situation. They both made good money during the boom years. But they also warned people as far back as 2013 that prices were nuts. They were wrong about timing. Prices went much higher for much longer than seemed rational. But they were not wrong about the fundamentals.

“We just live the honest life,” Butler said. “Maybe it’s not doing us any good, but we did live the honest life.”

Their message for 2026 is clear. It will be rough. The correction is not over. If you are waiting for next spring to be better, it might be much worse.

All the distortions are gone now. Foreign money. Low interest rates. COVID insanity. Student visa explosion. What is left is the simple question that was buried for over a decade.

Can somebody actually afford to buy this house?

For too many properties in Ontario, the answer is still no.

I hope you’re staying dry on this rainy day. Today, I want to discuss a property listing that has been on my mind for quite some time—not just because of its prolonged presence on the market, but because of the broader lessons it offers about real estate pitfalls.

What bothers me most is this: In the same neighborhood, countless houses have been listed and sold promptly. If they didn’t sell within a reasonable time, the listings were withdrawn—yet these two properties remain, defying the trend. Now, they risk becoming stigmatized listings—homes that buyers avoid simply because they’ve sat unsold for too long, sparking suspicions of hidden flaws or desperate sellers.

The listing in question (pictured) is a prime example of how overpromises, misplaced trust, and a lack of due diligence can turn a straightforward sale into a cautionary tale. Let’s break down why this property has struggled to sell—and what buyers and sellers can learn from its story.

The real estate market is often seen as a realm of opportunity, but it can also be fraught with pitfalls—especially when trust is misplaced, and due diligence is neglected. A recent listing in my neighborhood serves as a cautionary tale, revealing critical lessons for buyers, sellers, and investors alike.

The Story of House #56 and #58: A Case of Failed Promises

The property in question—House #56—is currently listed by a well-known realty brokerage that boldly claims, “We’ll buy the property if it doesn’t sell!” At first glance, this seems like a strong guarantee, but the history of this property (and its neighbor, House #58) tells a different story.

Both houses belong to the same owner, who appears to be facing financial distress. House #58 was initially listed by a Muslim female realtor but remained unsold for over a year. The owner then switched to another Muslim realtor who markets himself as a “real estate don” with a promise to purchase unsold listings. Yet, even under this Celebrity Realtor’s (he loves to be called it) representation, House #58 failed to sell and was eventually pulled off the market.

Now, House #56 has been listed for over six months with no success. The prolonged market exposure has likely stigmatized the property—buyers are wary of homes with long listing histories, assuming there must be something wrong.

The Big Question: Does this Celebrity Realtor Really Buy Unsold Listings?

This Celebrity Realtor’s promise raises skepticism. If his guarantee were genuine, why hasn’t he purchased House #56 or #58? The reality is that such claims may be more marketing gimmick than solid assurance. Sellers should be cautious of bold guarantees that aren’t backed by clear contractual terms.

Key Lessons for Buyers and Sellers

1. Don’t Choose an Agent Based on Religion, Culture, or Community Ties

The owner of Houses #56 and #58 switched from one Muslim realtor to another, possibly assuming shared background would ensure better service. However, competence, market knowledge, and negotiation skills matter far more than shared ethnicity or faith. Other homes in the same neighborhood are selling—just not these two.

Lesson: Hire professionals based on track record, not personal connections.

A dangerous trend in real estate is the “closed network”—where a realtor refers clients to their preferred mortgage broker, home inspector, or lawyer. While convenient, this can lead to conflicts of interest.

Inspection Failures: A Toronto buyer sued their realtor after discovering severe defects in their home—defects that the realtor’s “trusted inspector” had missed.

Mortgage Traps: Some buyers with strong finances were steered into expensive private mortgages by brokers within the same network, costing them thousands in extra interest.

Lesson: Always seek independent professionals. Never skip a proper inspection or rely solely on referrals from your agent.

3. Verify Everything—Don’t Blindly Trust

Many buyers, especially first-timers, assume that because their realtor is a friend or community member, they won’t be misled. Unfortunately, financial incentives can override loyalty.

Skipping Inspections: Buyers spending millions on a home often hesitate to spend $300 on an inspection, believing their agent’s assurances.

Ignoring Legal Docs: Some forego condo status certificates or land surveys, only to face costly surprises later.

Lesson: Trust, but verify. Pay for inspections, review condo documents, and get a land survey. These small costs prevent massive losses.

Final Thoughts: Protect Yourself in a Complex Market

The real estate market is cooling in many areas, and sellers must price realistically while buyers must conduct thorough due diligence. The saga of House #56 and #58 highlights:

Overpromises mean little without proof.

Networks can be traps if not scrutinized.

Independent verification is non-negotiable.

Whether buying or selling, approach real estate with a business mindset—not blind trust. The right professionals will welcome your diligence rather than discourage it.The Bottom Line: If a deal seems too reliant on personal connections rather than hard facts, step back and reassess. Your financial future depends on it.