I recently watched a podcast by mortgage expert Ron Butler discussing a troubling trend in Ontario’s real estate market: home purchase failures have increased by 500% compared to pre-COVID levels.

That number should make all of us pause.

What Is a “Purchase Failure”?

A purchase failure happens when a buyer signs a contract to buy a home — new construction or resale — but cannot close the deal on the agreed closing date.

In simple terms: The buyer doesn’t have the money or cannot secure the mortgage needed to complete the purchase.

Before COVID, less than 1% of purchases failed. Today, that number is reportedly around 5% — and in new construction, some estimate it could be much higher.

Why Are Deals Falling Apart?

There are several major reasons:

1. Appraisal Problems (Especially New Construction)

Many buyers purchased pre-construction homes or condos in 2021–2022 at peak prices. Now that projects are completing:

Market values have dropped.

Appraisals are coming in far below the original purchase price.

Buyers must cover the difference in cash.

If you bought at $1.95M and the appraisal comes in at $1.525M, that’s a $400,000 gap you must cover. Many simply can’t.

2. Condo Market Reality

Some buyers purchased condos years ago at inflated prices, expecting appreciation or easy rental income. Today:

Comparable units are selling for less.

Higher interest rates mean negative monthly cash flow.

Rental income often doesn’t cover mortgage payments.

Some buyers are choosing to walk away from large deposits rather than close on a losing investment.

3. Mortgage Qualification Issues

In resale markets, failures are happening because:

Buyers couldn’t sell their existing home for the expected price.

Income was overstated or improperly assessed.

Job losses occurred before closing.

Buyers assumed pre-approvals guaranteed final approval (they don’t).

As Ron Butler bluntly stated: “The buyer doesn’t have the money.”

Why This Matters to Our Community

This is not about panic. It’s about awareness.

When purchase failures rise:

Sellers face uncertainty.

Builders face stress.

Buyers risk losing deposits.

Legal disputes increase.

Financing becomes stricter.

We are entering a market where leverage cuts both ways.

For years, rising prices hid risk. Today, falling values expose it.

If You’re Buying or Investing, Be Careful

Before signing anything:

Get a fully verified mortgage approval (not just a quick pre-qual).

Be conservative with projected sale prices.

Stress-test your finances at higher interest rates.

Understand appraisal risk.

Have liquidity reserves.

Read pre-construction contracts very carefully.

Speculation worked in a rising market. It is dangerous in a correcting one.

Final Thought

Real estate is not guaranteed to go up. It never was.

The goal is not to scare anyone — but to make sure our community members are informed. The people who survive market corrections are not the boldest. They are the most disciplined.

If you’re planning to buy, sell, or close on a property soon, now is the time to review your numbers carefully.

Toronto’s condo market is not experiencing a normal downturn. It’s going through a structural breakdown.

According to Urbanation data, by 2029 Toronto could see virtually no new condo completions. That sounds impossible in one of North America’s fastest-growing regions—but the numbers don’t lie. New condo sales in the GTA have collapsed to their lowest levels since 1991, despite today’s population and housing demand being dramatically higher.

This collapse isn’t random. It’s the failure of the investor-driven condo model.

For over a decade, most pre-construction condos weren’t built for families or end-users. They were built for investors. The model was simple: buy pre-construction, wait a few years, prices rise, rent it or flip it. That model only worked in a world of cheap money, rising prices, and investor optimism. That world is gone.

High interest rates, falling prices, and weaker rents have destroyed the economics of pre-construction investing. As investor demand disappears, the entire development pipeline shuts down.

And here’s the key reality: Pre-construction sales drive future construction. When sales collapse, housing starts collapse. When housing starts collapse, future supply disappears.

This is already happening across the GTA, with housing starts far below long-term averages. Even if demand returns tomorrow, supply cannot restart quickly—condo development is a multi-year process. Today’s sales collapse becomes tomorrow’s supply crisis.

This isn’t primarily about government taxes or red tape. Housing starts are falling across North America. This is a housing cycle problem, amplified in Toronto because the city became deeply dependent on speculative investor demand.

The economic impact will go far beyond housing. Construction jobs, trades, suppliers, engineers, and entire supply chains are affected. Housing doesn’t just reflect the economy — it drives it.

But this doesn’t mean prices will automatically surge in a few years. Future outcomes depend on uncertain factors: population growth, immigration, interest rates, economic conditions, and income growth. Anyone selling a simple “supply crash = guaranteed boom” story is oversimplifying reality.

The truth is simpler and more honest:

Toronto’s condo market has hit a breaking point. The investor model no longer works. The supply pipeline is shrinking. And the housing system is entering a painful but necessary reset.

What comes next won’t be shaped by hype — it will be shaped by fundamentals, policy, and economic reality.

Canada’s housing crisis is often discussed in absolutes: either prices will crash, or they will never fall; either governments must intervene more, or get out of the way entirely. But when we place recent market conditions alongside deeper structural critiques—like those raised on Angry Mortgage—a more complicated, and more honest, picture emerges.

A Short-Term Opening for Buyers

In the near term, there is a meaningful shift underway—particularly in markets like Toronto and Vancouver.

Sales volumes are historically low. Investor activity has largely evaporated. Pre-construction is stalled. Buyers who remain are mostly end users: families and individuals looking for a place to live, not to flip. This has quietly shifted leverage. Selection has improved. Negotiation is back. Sellers, not buyers, are adjusting expectations.

This does not mean we are at the “bottom,” nor does it mean prices cannot fall further. But for financially stable households—especially first-time buyers who were entirely shut out between 2020 and 2022—this is the most buyer-friendly environment in years.

Yet this short-term opening exists inside a housing system that remains fundamentally broken.

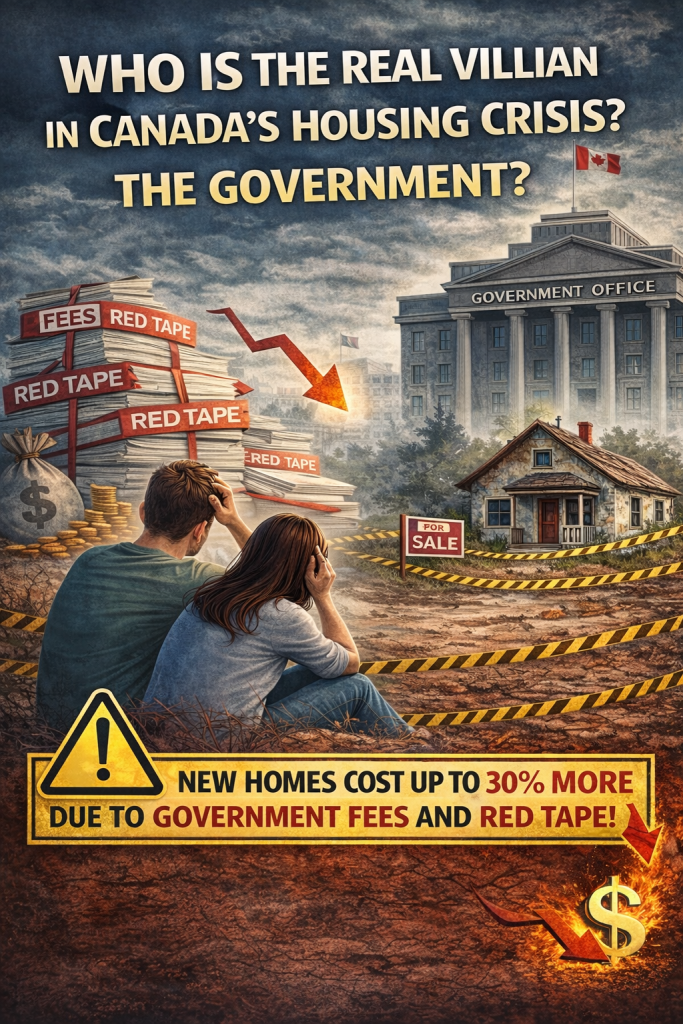

The Structural Problem: Housing as a Government Revenue Tool

As Ben Woodfinden argued on Angry Mortgage, the most under-discussed driver of unaffordability is not speculation alone, immigration alone, or even interest rates—but government cost-loading on new housing.

In cities like Toronto, as much as 30% of the cost of a new home is made up of development charges, fees, taxes, and levies. These are not marginal costs. They are embedded into the price of every unit, passed directly to buyers, and treated as a normal feature of governance.

Housing, in effect, has been taxed like a luxury good—while being rhetorically framed as a human necessity.

Layered on top is what Woodfinden calls the “Anglo disease”: a regulatory culture that makes building slow, adversarial, and legally dense. Years of approvals, consultant reports, appeals, and political veto points create scarcity by design. The result is not careful planning—it is paralysis.

This is how Canada ends up with 50-storey towers beside single-family zoning, and almost nothing in between.

The Missing Middle—and the Missing Social Contract

What ties these discussions together is not just economics, but expectations.

A generation of Canadians did what the social contract asked of them: education, work, saving, delayed gratification. Yet homeownership now requires top-1–2% household incomes in major cities. The promise that effort leads to stability has quietly collapsed.

That anger is not theoretical. It shows up in delayed families, longer commutes, overcrowding, and a growing sense that democracy responds faster to asset holders than to workers.

When young professionals earning $90,000–$100,000 cannot even imagine owning a modest home, something deeper than market cycles has failed.

So Where Does This Leave Us?

In the short run, today’s market offers cautious opportunity for buyers who are purchasing shelter, not status.

In the long run, affordability will not be restored without structural change:

Development charges must be rethought.

Zoning must allow mid-density housing where people already live.

Speed, not symbolism, must become the metric of housing policy.

More programs alone will not fix this. Nor will pretending the market can self-correct under the current regulatory load.

A Critical Outlook

Canada’s housing crisis is not caused by a single villain. It is the outcome of decades of policy choices that treated housing simultaneously as an investment vehicle, a revenue source, and a political risk to be avoided.

Buyers may find a window today—but unless governments stop profiting from scarcity while promising affordability, that window will close again.

The question is no longer whether housing is broken. It is whether we are willing to stop pretending we don’t know why.

The Hidden Debt Crisis: What’s Really Happening with Canadian Households in 2025

Based on insights from Doug Hoyes, leading consumer debt expert and co-founder of Hoyes Michalos

If you’ve been feeling financially squeezed lately, you’re not alone. A recent conversation between John Pasalis of MoveSmartly and Doug Hoyes, one of Canada’s foremost experts on consumer debt, reveals a troubling picture of what’s happening beneath the surface of our economy—and surprisingly, it might be worse than the statistics suggest.

The Numbers That Don’t Add Up

Here’s what’s puzzling experts: despite record-high debt levels, rising unemployment, and a challenging real estate market, consumer insolvencies in Ontario haven’t exploded the way many predicted. In fact, they’re only slightly higher than last year.

“What’s most amazing to me is they aren’t as high as I would expect them to be,” admits Hoyes, whose firm has been tracking insolvency trends for nearly 30 years.

So what’s really going on?

The Great Divide: Homeowners vs. Renters

The data reveals a stark reality about Canada’s two-tier economy. Back in 2011, about one-third of Hoyes’ clients were homeowners when they filed for insolvency. By August 2022, that number hit zero—the only time in the firm’s history.

Today, it’s crept back up to around 10%, but that’s still dramatically lower than historical norms.

Why the shift? It comes down to equity. If you bought a house decades—or even just years—ago, you’ve likely built substantial equity that acts as a financial buffer. Need to deal with credit card debt? Refinance, get a HELOC, or sell and pocket the difference.

But if you’re renting? You have no equity cushion whatsoever. You’re the most vulnerable to job loss, inflation, and rising costs.

The Precon Time Bomb

One of the most concerning trends Hoyes discusses is the wave of preconstruction condos that buyers can’t close on. Here’s how the crisis unfolds:

Buyer purchases a precon condo in 2022 for $1 million with a $100,000 deposit

Property finally ready for occupancy in 2024-2025

Current appraisal: $700,000-$800,000

Bank refuses to provide a $900,000 mortgage on a $700,000 property

Buyer cannot close

Unlike the United States, Canadian buyers have full recourse—they can’t simply walk away. Builders can sue for their losses, potentially going after your other assets, including your primary residence.

“We’ve got this massive amount of pent-up problems—precons that aren’t closing that have not yet resulted in hardly any bankruptcies because the legal process hasn’t consummated yet,” Hoyes explains. “That’ll be a story for 2026, probably into 2027.”

Why Banks Are Playing the Waiting Game

Another revelation: many borrowers have stopped making mortgage payments on rental properties, yet banks aren’t aggressively pursuing power of sale proceedings.

Hoyes shares the story of a client who stopped paying her rental property mortgage in August—and months later, the bank had done virtually nothing beyond sending a letter.

The theory? Banks may be slow-walking foreclosures to avoid flooding the market with inventory, which would drive prices down further and crystallize everyone’s losses. With many borrowers in similar situations, a wave of simultaneous foreclosures could trigger a broader market collapse.

The Rental Property Trap

The mathematics of rental properties have turned brutal for many investors:

Monthly shortfall of $1,000-$2,000 was common but manageable when prices were rising $100,000+ annually

Investors borrowed from HELOCs and unsecured lines of credit to cover the gap

After 2-3 years of monthly shortfalls, credit lines are maxed out

Property values have declined or stagnated

No equity to refinance

No cash flow to continue

“Unless you’re the federal government, you cannot run a deficit every month forever and not experience the consequences,” Hoyes notes bluntly.

A Generation Locked Out

Perhaps most troubling is Hoyes’ explanation of why gambling, risky investing, and speculative real estate purchases have exploded among younger Canadians:

“If you are 25 years old today, you know that there is no hope that you will ever be able to buy a house unless your parents give you the money. There is no mathematical way you can do it.”

He paints a stark picture: making $80,000-$90,000 annually leaves about $50,000-$60,000 after tax—barely enough to cover living expenses in major Canadian cities, let alone save $200,000 for a down payment.

This sense of hopelessness has driven many toward high-risk strategies: gambling apps, cryptocurrency, options trading, and yes—speculative real estate purchases.

The Leverage Trap

Real estate’s appeal as a get-ahead strategy is rooted in leverage. With just 5% down, a 10% increase in property value triples your initial investment (on paper). You can’t get that kind of leverage in the stock market, where margin requirements are typically 50% or higher.

But leverage cuts both ways. When property values decline by 20-30%, highly leveraged buyers don’t just lose their down payment—they end up owing substantially more than their property is worth.

Warning Signs Ahead

Several trends suggest 2026 could bring more financial pain:

Rising bankruptcy rates: The percentage of bankruptcies versus consumer proposals is increasing because people simply don’t have enough income to make payment plans work

Debt too high to restructure: Some people now owe so much (particularly on failed precon purchases) that they exceed the $250,000 limit for consumer proposals and must file bankruptcy instead

Shrinking cash flow: Unlike previous decades where inflation gradually made fixed payment plans easier over time, today’s rising costs mean those $300 monthly proposal payments get harder each year, not easier

Precon lawsuit wave: As builders begin quantifying their losses and pursuing legal action against buyers who couldn’t close, a wave of judgments and garnishments is likely coming

What You Can Do

Whether you’re a homeowner or renter, Hoyes offers practical advice:

Take inventory honestly:

List all assets (be realistic about current market values)

List all debts with amounts, interest rates, and minimum payments

Calculate your actual monthly cash flow

Be realistic about solutions:

Can you increase income (part-time work, side gig)?

Can you reduce expenses meaningfully?

If you’re a homeowner, does selling and renting make sense?

Could you move in with family temporarily?

Get professional advice early: “Debt problems do not get better on their own magically. It’s just not how it works,” Hoyes emphasizes.

If you’re overwhelmed, speak with a licensed insolvency trustee—they’re the only professionals licensed by the federal government to administer proposals and bankruptcies. About three-quarters of people who contact them end up finding solutions without filing insolvency.

The Bottom Line

We’re in a strange economic moment where the full extent of financial distress hasn’t yet shown up in official statistics. Banks are delaying foreclosures, legal processes are grinding slowly, and many people are simply kicking the can down the road.

But as Hoyes makes clear, this can’t continue indefinitely. The mathematical reality will eventually catch up.

For those feeling squeezed: you’re not imagining it, you’re not alone, and there are steps you can take before things become crisis-level. The key is acting before you’ve exhausted all your options.

Before you buy a house in Canada in general and Greater Toronto Area (GTA) in particular, you need to know about a housing bubble. The reason I keep saying do not just jump into the market yet is because the real estate practitioners are worried whether the bubble is going to burst anytime soon. Remember housing price was at the peak in 2022 and the price was checked with the interest rate rise. It is not that the bubble is burst yet, it is just controlled. It is important to understand it. Let’s talk about what it is.

A housing bubble happens when housing prices skyrocket, and real estate values become so unsustainably high that eventually the bubble bursts. Housing prices are disconnected from the “intrinsic property values.” Intrinsic property values are prices based on economic factors like income levels, rental costs, and other things that traditionally influence property values. Skyrocketing housing bubble prices occur when several things happen at once. Some of the contributing factors are: Speculation, Limited Housing, Interest Rates, Mortgage Debts, and Increased Development.

“If inflation continues to ease, and our confidence that inflation is headed sustainably to the 2-per-cent target continues to increase, it is reasonable to expect further cuts to our policy interest rate. But we are taking our interest rate decisions one meeting at a time.” Mr. Macklem said. The Bank of Canada is the first G7 central bank to start easing monetary policy. The European Central Bank is expected to follow suit on Thursday, while the U.S. Federal Reserve, which is dealing with a stronger economy and more stubborn inflation, is expected to hold off rate cuts until later in the year.

The next meeting is on July 24, six weeks from now. This interest rate cut is like “finally, the interest rate is not going to increase.” Nothing more than that. Looks like this rate cut is not going to bring any momentum in a near future. Since the current inventory dictates price of a house for at least 90 days, there is more than enough inventory in the GTA housing market. Based on the current listing, free hold market may go up whereas condo market will stay same or go down until the current inventory is cleared up since there is too much inventory in the condo market.